Written by Yanis Kharchafi

Written by Yanis KharchafiFiduciary Expert in Training

HEC/AFA/IAF Graduate

How does retirement work for the freelancers? AVS, LPP and 3rd pillar

Introduction

Have you decided to make a career change and throw yourself headfirst into an entrepreneurial adventure? Have you already had a chance to read our complete guide to starting your own business?

In this 2nd guide, we’re going to focus more specifically on retirement for the self-employed, so that you can better anticipate the pensions and capital you may receive once your career is over.

That leaves you with just one essential guide to read before going any further: accounting and taxation for the self-employed.

The line-up:

The first pillar for the self-employed: AVS & AI

How do I choose my AVS compensation fund?

I don’t know if this is good news, but a freelancer, just like an employee, is obliged to join the AVS. There are several AVS compensation funds, and they all work in the same way. So, the best decision is probably just to choose the one that covers your canton.

- AVS compensation funds for the canton of Vaud : https://www.caisseavsvaud.ch/fr/Accueil/Caisse-cantonale-vaudoise-de-compensation-AVS.html

- AVS compensation funds for the canton of Geneva (OCAS) : https://www.ocas.ch/

- AVS compensation funds for the canton of Valais : https://www.vs.ch/web/avs

You will need to fill in their questionnaire and prove the strength of your business plan.

How does the first pillar work for self-employed individuals?

Step 1 – Provide an estimate of income and salary subject to AVS contributions

Let’s assume the AVS has officially recognised your self-employed status. Your very first step is to submit to your AVS fund an estimate of the income subject to social security contributions. In practice, this means forecasting your expected financial results by estimating as accurately as possible the expenses and revenue for the coming year.

This estimate will allow you to determine your projected profit subject to AVS contributions — a figure you will then communicate to your compensation office.

Based on this information, the AVS will calculate your provisional contributions (see below) and will send you quarterly advance invoices corresponding to your estimated amounts.

Important note: this procedure mainly applies to self-employed individuals working alone, without employees.

If you plan to hire staff, you must also communicate the agreed gross salaries of each employee to the AVS. The compensation office will then include both the employee and employer AVS contributions in the quarterly instalments invoiced to your sole proprietorship.

Step 2 – Final contribution settlement in year N + 1

Because the amounts indicated in the previous step are only estimates, you will need to prepare your final annual accounts at the beginning of the following year and submit them to your AVS fund. The fund will then issue a final and accurate settlement. Two scenarios may occur:

- Your advance payments were too high, in which case the AVS will refund the difference — often with advantageous interest.

- Your advance payments were too low, meaning you will need to pay the remaining balance.

Step 3 – Setting the new advance payments

And then the cycle starts again! Once your annual accounts have been submitted and the final AVS contributions have been established, these definitive amounts will normally serve as the basis for calculating the new provisional instalments for the following year.

The year after that, you will again prepare your actual annual accounts, send the results to the AVS… and so the process continues from one year to the next.

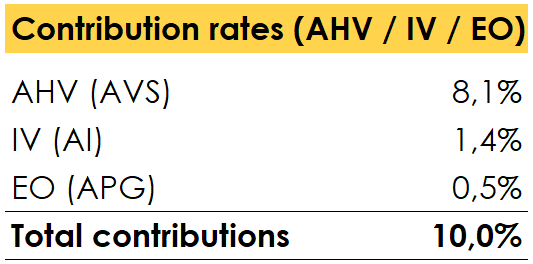

AVS contributions

Contributions for the self-employed are slightly different from those for employees. The difference lies in three points:

– There are no unemployment contributions

– There are no accident insurance contributions.

– As you no longer have an employer, you will be responsible for all social security contributions.

The contributions (effective from January 1, 2025) can be summed up in 3 points, as shown in this small table:

However, if your income does not exceed CHF 60,500 during the year, the contribution rates are reduced accordingly.

How do AVS pensions work?

You’ve contributed to the AVS for many years without ever hesitating, and now you’re thinking about slowing down? Good news: the AVS will pay you a lifetime pension, starting on the very first day of your retirement and continuing for the rest of your life.

Since the amounts and calculation methods are exactly the same as for salaried employees, I strongly encourage you to take a look at our detailed article on how AVS pensions are calculated. There, you’ll find all the information you need to determine the age at which you’ll be able to retire, especially following the implementation of the “AVS 21” reform.

But for those who don’t have the energy to click on that link, here’s a quick summary to give you a solid overview:

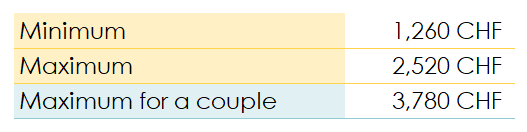

Starting in 2025, AVS pensions will range from CHF 1,260 to CHF 2,520 per month. Where you fall within that range depends on your average annual income subject to AVS contributions. If you contributed throughout your career on an average annual income of CHF 90,720 or more, you’ll be entitled to the maximum pension.

To know exactly where you stand, simply look for the table known as “Scale 44”.

I can already guess your next question: “Okay, but what if I started working late? Are three years of work enough to receive CHF 2,000 per month for life?” Obviously not. Each missing year of contributions from age 21 onward reduces your pension by 2.27%.

So, if you begin contributing at age 50 and work until 65, you will have accumulated 15 years of contributions, but also 29 years of gaps. This means your pension will be reduced by 29 × 2.27%, which amounts to roughly 66%.

One last helpful detail: the AVS system works very much like the French pension system, as it is based on solidarity rather than capitalization. Employees, self-employed individuals, and even people without gainful employment all contribute to the AVS, and these contributions are used to pay retirees’ pensions in the same year. In other words, your contributions do not form a personal retirement pot; instead, they are immediately redistributed to current beneficiaries.

The second pillar for the self-employed : BVG / UVG

If you’ve read our article on AVS pensions, you’ve probably realized that while it’s certainly reassuring to receive a guaranteed lifelong pension, the amounts are overall rather disappointing. Unfortunately, the first pillar alone won’t be enough to cover all your financial needs in retirement.

Being self-employed means spending your entire career finding enough clients to generate the income you need for your daily life. But it also means that, aside from the AVS, no one will be there to support you financially once you reach retirement age. In Switzerland, it’s essential for self-employed people to anticipate this phase by putting sufficient measures in place to secure their financial future — whether through personal investments, by planning for the potential sale of their business, or by voluntarily joining (and I insist on the word voluntarily) a second-pillar pension fund.

Choosing to voluntarily join a second-pillar scheme is a simple and reassuring way to bring your level of financial security closer to that of an employee. Your pension fund will then be responsible for collecting your contributions, investing them to build your own retirement capital, and — most importantly — allowing you, when the time comes, to choose between receiving a lifelong pension or withdrawing all your contributions and accumulated interest as a lump-sum payment.

The 2nd pillar / LPP in the broad sense :

Unlike the first pillar, the LPP/BVG is a capital that belongs to you and will never be distributed to other insured persons. It is essentially made up of :

– Voluntary contributions from the insured

– Interest and returns on your BVG capital

– The division of BVG capital after a divorce

As long as you are affiliated to the 2nd pillar, your BVG capital will never stop growing until the day you retire (or if you claim another reason for withdrawing your 2nd pillar capital).

When you retire, your capital can either :

– Be withdrawn in the form of an annuity for life as for the first pillar

– be withdrawn as a lump sum

– Divided into an annuity and a capital sum

We have also explained 2nd pillar pensions and capital in another article.

The 2nd pillar: How does the 2nd pillar work for self-employed persons in Switzerland?

As this is an option and not an obligation, the freelancers are entitled to ask themselves: should I join the 2nd pillar or would it be better to keep this income to develop my business or simply to treat myself?

This is not a question to which there is a simple answer, but before giving you some advantages here is a brief reminder of how the 2nd pillar works for the self-employed:

Depending on your salary and the interest paid, your second pillar capital can be split into two parts:

– The mandatory part

– The non-mandatory part

Mandatory LPP: the bare minimum

The 2nd Pillar Act sets out all the legal minimums:

Salary on which you will pay contributions

Depending on your age, the minimum contributions are as follows

o 7% aged 25 to 34

o 10% aged 35 to 44

o 15% aged 45 to 54

o 18% aged 55 to 64 for women / 65 for men (before the new AVS 21 standards came into force)

Be careful — this rule applies both to employees and to the institution that accepts all Swiss self-employed workers, namely the “Fondation Institution Supplétive.” However, because affiliation to the second pillar is optional for the self-employed, most institutions offering this type of coverage have set contribution rates that may differ slightly from the ones mentioned above.

For example, it’s quite common to come across institutions that, instead of using four age brackets, offer only two, splitting your career into two major periods:

- Ages 25 to 44: 10%

- Ages 45 to 65: 15%

These rates are, of course, only indicative. To obtain a more accurate estimate tailored to your situation, I strongly recommend selecting two or three institutions likely to accept you and asking them for detailed offers so you can compare their pension plans. If needed, FBKConseils can also support you in this process by helping you analyze and compare the proposals you receive.

Interest rate

The more contributions you pay, the higher your capital will be. In addition to the contributions, your pension fund will invest your money in the markets according to their rules and do its best to make your capital grow from year to year. On the mandatory part of the contributions, annual interest of 1% is guaranteed. Interest rates vary between 0% and 6%, depending on the quality of the asset management. This capital will grow every year thanks to the investments made by your pension fund. On the mandatory portion, they will be required to pay you 1.25% interest for the year 2025. This rate changes from year to year.

Mandatory BVG/LPP: A tailor-made 2nd pillar

If you have followed this article carefully, you will have seen that there are :

– Minimum contribution rates

– Minimum interest: 1.25%.

– Maximum LPP/BVG insured salary: CHF 90,720

Together, these represent the mandatory part of your 2nd pillar.

But the second pillar offers the possibility of bending the rules by increasing (again, voluntarily) contribution rates and insured salary. The goal? To contribute as much as possible in order to deduct as much as possible. You will have the option of increasing your salary up to CHF 90,720 and contributing a maximum of 25% of your income. Now you know how you are going to contribute and the options available to you, but you still don’t really know what the point is? So let’s continue with that.

2nd pillar tax benefits

In addition to insurance and coverage needs, the second pillar can be a great tax reducer because all risk contributions (disability and death) and savings contributions (retirement) are tax-deductible. In other words, all of your contributions will be tax-deductible. It’s roughly as if you were paying yourself a salary that would not be subject to income tax. Considering that taxes range from 10% to 40%, the savings (excluding interest) could be very significant.

Interesting, isn’t it?

As well as not being taxed, the 2nd pillar has other aims besides saving tax. It also provides protection against 3 significant risks:

– Risk of death

– Risk of disability

– Provide you with a decent pension in addition to the 1st pillar.

Retirement, disability and death cover

At this stage, the workings of the second pillar should now feel much clearer. You now have a precise idea of the contributions you can make and deduct from your taxable income, as well as the potential future capital or pension it could provide. But be careful: the second pillar is not just a tool to optimize your taxes or supplement your first-pillar pension. It also plays a crucial role in protecting you against life’s uncertainties, particularly in the event of death or disability.

When you’re employed by a company, these are questions you rarely ask yourself, generally assuming that everything is already covered by law or through mandatory insurance. While this assumption is unfortunately risky for everyone, it is even more dangerous for a self-employed person, who cannot rely on any protection other than the first pillar. You can probably see where this is going: in addition to its retirement component, the second pillar provides highly valuable coverage against major risks, which may include:

- Disability pension

- Child’s disability pension

- Lump-sum death benefits

- Widow’s or widower’s pension

- Orphan’s pension

Another major advantage of the second pillar, compared with alternatives such as the third pillar A or B, is its attractive cost. In fact, death and disability coverage obtained through a pension fund gives you access to the same protections, but often at a price two to three times lower than what traditional private insurers typically charge.

Who will cover your income in case of accident or illness when you’re self-employed?

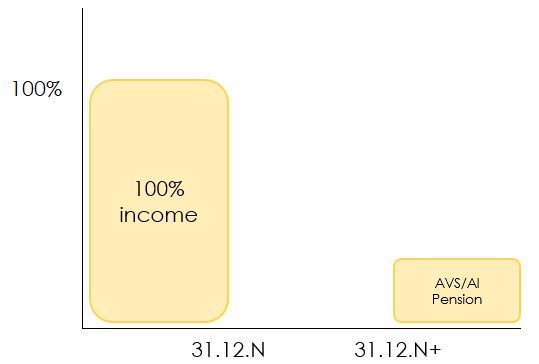

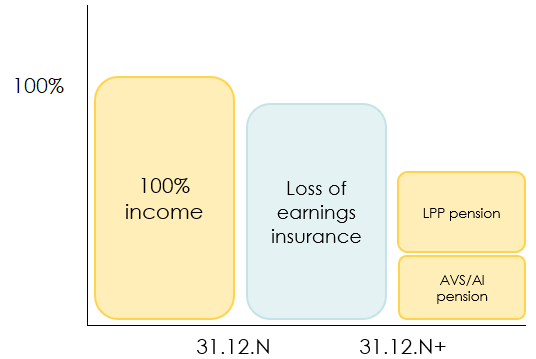

Let’s take the example of a self-employed person who voluntarily chooses to subscribe only to the strict legal minimum. You are therefore affiliated solely with the AVS, when a sudden accident occurs on December 31st. You suffer a serious fall and, unfortunately, you are unable to work without knowing exactly when you might be able to resume your activity. Here’s what your financial situation would look like:

This chart clearly shows that between the day of your accident and the day when the AVS officially recognizes you as “disabled,” a period of up to 720 days (that is, two years) may pass. During this time, you will have to cover your financial needs entirely on your own. Then, once you are officially recognized as disabled, and depending on your degree of disability, you will only receive a portion of the AVS pension mentioned earlier. A harsh reality, isn’t it?

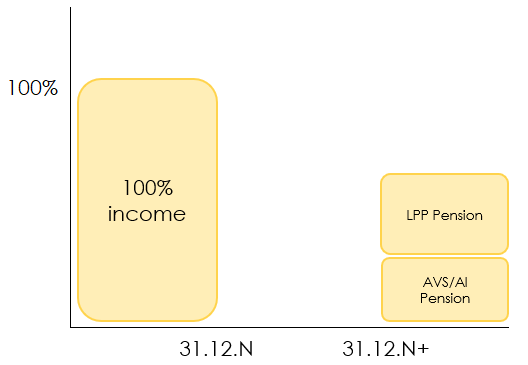

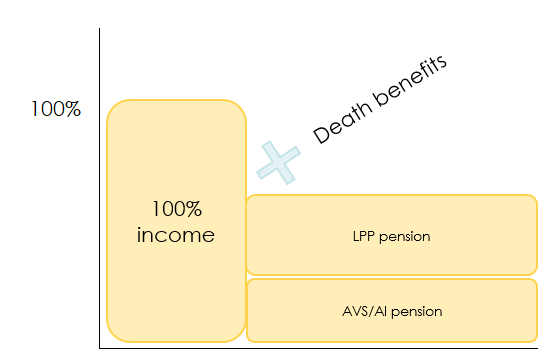

Now, let’s take a look at how things would change if you had voluntarily joined a second-pillar pension plan:

The main difference here lies in the addition, after the initial 720-day period, of an additional pension paid by your second-pillar plan. This typically corresponds to a percentage of your insured salary. However, it’s important to note that the financial gap during the first two years of disability remains.

So the natural question arises: how can you secure your income during this period? The answer: accident insurance (LAA) and daily sickness benefit insurance. These two insurances, optional as long as you have no employees, are specifically designed to cover this interim period until the compensation fund takes over. While these insurances represent a non-negligible cost, they allow you—depending on your investment capacity and the risks you wish to cover—to secure a significant portion of your income during these critical first two years.

In conclusion, I would say that subscribing to all these insurances is indeed not mandatory. In fact, I’ll be the first to admit that I’m not particularly fond of insurances or insurers. However, it is even riskier not to fully understand the financial stakes illustrated in these charts. Being self-employed inherently involves taking on some risk—but that risk must be carefully calculated and managed.

Who will cover your household income in the event of death?

Discussing disability is already difficult, but talking about death is even more so. I’ll therefore be brief and concise.

No one likes to bring up this topic, but the reality is that death is part of life, and unfortunately, this risk does not spare the self-employed. What actually happens if you are self-employed and pass away?

I won’t call it “good news”—obviously inappropriate in this context—but the positive aspect compared to disability is that in the case of death, there is no waiting period: coverage is immediate. From the very first day after your passing, the first pillar (AHV/AVS) can pay survivor’s pensions to your spouse and orphan’s pensions, depending on the family situation and the age of the beneficiaries.

In addition to first-pillar benefits, your second pillar (BVG/LPP), if you are enrolled, can also pay death benefits and pensions, depending on the contract and the pension fund you have chosen.

Before moving on to the 3rd pillar, there’s one last question on my lips: how do you choose your 2nd pillar?

The 2nd pillar: How do you open a 2nd pillar and with whom?

If you have weighed up the pros and cons and would like to join a 2nd pillar scheme, there are 3 possible options:

– Pension funds in your field of activity

Some pension funds are specialised in a specific area (doctor, lawyer, artist, etc.). If one of these areas applies to you, you should first contact them to obtain a tailor-made solution that best suits your needs.

– Your employees’ pension funds

If you employ staff, you will also be able to apply for membership of their institution, even if it is not part of your business sector.

– The supplementary institution

This is a public institution that allows any self-employed person to join. This will never be the most suitable solution in terms of cost and options, but it does offer cover close to the legal minimums.

It’s time to switch to the 3rd pillar: private, unrestricted, A, B pension provision? Let’s get started!

The 3rd pillar for the self-employed

There are countless articles on the 3rd pillar that we have written or that you can find on other sites (not as good as ours).

- How much can we save in taxes thanks to the pillar 3?

- Pillar 3A at the bank or with an insurance, what is the best choice?

But here we are going to focus more specifically on the 3rd pillar for the self-employed.

I suggest we start with Pillar 3A.

The 3rd pillar A: Private or tied pension provision

This is the same 3rd pillar A opened by an employed person. It is a bank account or insurance policy into which you can put a certain amount each year to save for your retirement.

The big and only difference comes from the possible amounts.

– The 3rd pillar if you are not affiliated to the 2nd pillar

In your self-employed activity you did not wish to affiliate to a 2nd pillar, so you can contribute 20% of your income or a maximum of CHF 36,688 in 2025 and 2026 to your 3rd pillar.

– The 3rd pillar if you are affiliated to the 2nd pillar

If you are self-employed and wish to join the 2nd pillar, you can deduct 20% of your income or a maximum of CHF 7,258 in 2025 and 2026 from your 3rd pillar.

There is no other difference.

Our advice? In the first few years, it might be a good idea to opt for a 3rd pillar A bank account (and not an insurance policy!). That way, you avoid the problems associated with buy-back values and, depending on your budget, you can invest the amount of your choice with no obligation from one year to the next. Once you have started your business and your income are more certain, the 2nd pillar combined with the 3rd pillar could be the best option.

3rd pillar B: Unrestricted pension provision

The first important thing to know is that, unlike the 3rd pillar A, the 3rd pillar B is only a solution offered by insurance companies. It cannot be taken out with a bank. What’s more, except in certain cantons, it is not really deductible from municipal and cantonal tax (ICC).

As a result, it is generally not a good solution for saving tax. Nevertheless, even if it seems to have only disadvantages right now, the 3rd pillar B can in some cases be an effective insurance.

The 3rd pillar B, more commonly known as life insurance, allows you, while still alive (and in good health), to protect yourself against death and invalidity in addition to the 2nd pillar, with much greater flexibility in terms of beneficiaries. The 2nd pillar allows you to cover family members only (at a lower cost). You won’t have any leeway over who is insured, and capital and pensions will be paid out in a very specific order.

With the 3rd pillar B, on the other hand, you decide without limit who will receive what and in which situation. It is the perfect tool for protecting your partners and your company in the event of a major problem. It allows you to free up capital to keep your business running when the going gets tough.

I think we’ve given you enough information about retirement for the self-employed for today. You should now be able to understand what’s at stake and, above all, ask yourself the right questions about your future.

Even if, when you start out as a self-employed person, the last problem you seem to have is the very distant future, I can assure you that it’s very important to keep all this in the back of your mind and to take the necessary steps as soon as possible so that you can complete your project with a light heart.

How can FBKConseils support you with your independent business?

Starting out as an independent professional is a demanding journey. While we can’t choose your field of activity, FBKConseils is here to assist you with all the other essential aspects. Creating, managing, and making an independent business profitable requires knowledge and tailored support. Here’s how we can help:

An initial introductory meeting

Sometimes, a simple conversation is enough to dispel doubts. We offer a 20-minute free consultation designed to address your essential questions and lay the groundwork for your project. This meeting is the perfect opportunity to clarify your ideas and plan the next steps of your entrepreneurial journey.

In-Depth advisory sessions

Once your project is launched, it’s often necessary to tackle complex topics such as:

- Solutions to prepare your retirement, including subscribing to a 2nd pillar plan.

- Tax optimization strategies to maximize your income.

- Financial simulations to better anticipate the costs and benefits of your business.

At FBKConseils, we organize personalized advisory sessions to explore these questions in depth and provide answers tailored to your situation.

Accounting, Tax filing, and VAT management

As an independent professional, you’ll often face administrative formalities that can feel time-consuming. FBKConseils is here to ease your burden:

- We take care of your business accounting.

- We assist with your annual tax returns.

- We manage your VAT-related procedures, if applicable.

With our support, you can focus on what truly matters: growing your business.

With FBKConseils, you’re never alone when facing the challenges of entrepreneurship. Contact us today to discover how we can support you at every step of your journey.