Written by Yanis Kharchafi

Written by Yanis KharchafiFiduciary Expert in Training

HEC/AFA/IAF Graduate

What are the tax implications of your real estate properties held abroad?

Introduction

For several years now, we’ve been publishing a series of articles designed to help you better understand your taxes and the Swiss tax system. You can visit our Taxes page to find reliable tax information specific to your canton.

This article came about over time, as we realized that a large portion of our clients are foreign residents who, outside Switzerland, already own real estate property. Upon moving here, many choose to keep that property often as a secondary residence or a rental investment and rarely decide to sell it.

With this in mind, we decided to write this article to explain the Swiss tax implications related to owning real estate located abroad, which, at first glance, seems to be taxed only in its country of origin.

Rest assured, there’s something useful here for everyone: we’ll review situations of direct ownership (Part 1), bare ownership, and property companies (Part 2) such as SCIs or LMNP status for our French readers.

Buckle up I’ll do my best to keep this article clear and easy to follow, even though it covers many important tax concepts.

The line-up:

I decided to start with those who have bought, inherited, or directly invested in real estate located outside Switzerland, without using any complex structures. Let’s say that in your case, the situation is straightforward and crystal clear there’s no room for doubt.

Do I have to declare my property in Switzerland or only abroad?

No need to overcomplicate things the rule is simple: you must declare your real estate property both in your Swiss tax return and in the country where the property is located. Easy, right?

If you own a property, it must be reported for tax purposes in both countries.

The same applies the other way around: if you own a property in Switzerland but are a tax resident elsewhere (for example, in France), you will still need to file a tax declaration in Switzerland.

Where should I pay taxes on my foreign real estate?

For real estate – to distinguish from movable assets and revenues such as shares, bonds, dividends, coupons, etc… taxes are incurred where the property is located. If you rent your apartment in Divonne, then you will have to declare it together with the income it generates both in Switzerland and in France, but France will tax it all.

Foreign Real Estate — What Must Be Declared in Switzerland?

One question always comes up around the table: why should we declare our real estate located outside Switzerland, especially when it won’t actually be taxed here? Doesn’t that go against international tax rules? And above all, isn’t there a risk of double taxation?

The answer is rarely satisfying and often misunderstood but the facts are clear: yes, your foreign properties must be included in your Swiss tax return, no, they won’t be directly taxed in Switzerland, and yes, they will still affect your overall Swiss tax burden.

To understand why, let’s start by revisiting the basics of the Swiss tax system. Switzerland remains one of the few European countries that still levies both a wealth tax and an income tax. This distinction is crucial for what follows.

Indeed, as soon as you own property abroad, both types of taxes will be impacted.

So, let’s dive right in by first explaining what exactly needs to be reported in your Swiss tax return, and then detailing how this information will concretely influence your tax liability in Switzerland.

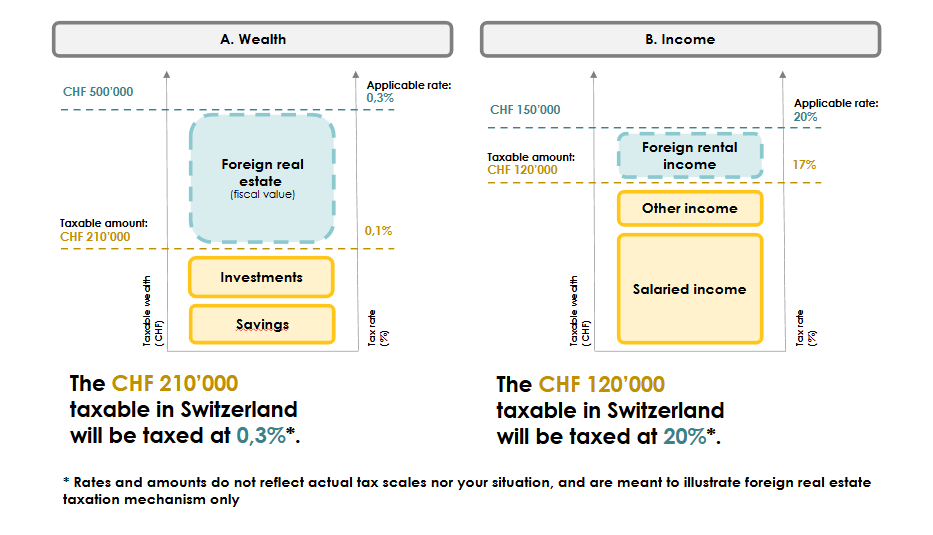

Wealth tax : The fiscal value of the real estate

No matter its type (second home, investment property, family house) you must disclose its so-called fiscal value. The tax authorities will refer to this indicator to assess your patrimony and consequently to define your tax rate.

And how do you define this tax value? Not easy to answer… Depending on your canton of residence, you will be subject to more or less strict rules:

Option 1: A tax certificate from the country where your property is located

In some countries, you can obtain the tax value of your property from the local authorities. If this is the case for you, we suggest that you try to use it, as there is a good chance that it will be much lower than option 2.

Option 2: Valuation based on purchase price

If you don’t have a tax certificate, you will have to start from the purchase price in most cantons and then you will be entitled either to an allowance, as in Geneva, or to a flat-rate reduction, as in the canton of Vaud.

Income Tax — Rental Income or Imputed Rental Value

I’m quite certain that even those who don’t yet have the right to vote in Switzerland have heard about the referendum on the imputed rental value.

This major tax reform sparked countless debates since the end of 2025 and ultimately resulted in the abolition of the imputed rental value starting in 2028.

I’m starting here because, in Switzerland at least until this new law takes effect there is no such thing as a property, whether located in Switzerland or abroad, that doesn’t generate income. In one way or another, every property must produce taxable income.

That’s precisely why we have an imputed rental value for properties used by their owners (such as holiday homes), and actual rental income for those that are rented out.

And the same logic applies to properties located abroad.

Imputed Rental Value

If you’ve decided not to rent out your holiday home and prefer to enjoy it both in winter and summer, you’ll need to calculate a “fictional rent” to add to your taxable income whether you like it or not.

At first glance, this may seem completely absurd, but the imputed rental value does have a purpose: it’s thanks to this mechanism that you can still deduct maintenance expenses. Without it, those deductions would simply disappear.

Now, the question is: how do you calculate this imputed rental value?

As is often the case in Switzerland, it depends on your canton.

While the principle of declaring an imputed rental value falls under federal law, the method of calculation is determined by cantonal law.

To give you some practical guidance, here are the rules applied in the two most common cantons:

- In the Canton of Vaud: the imputed rental value equals 6% of the property’s tax value (or fiscal estimate). Simply multiply that amount by 6%.

- In the Canton of Geneva: the imputed rental value equals 4.5% of the tax value. However, unlike Vaud, Geneva does not allow maintenance expenses to be deducted on this basis.

If you’d like a more accurate estimate, the easiest solution is to contact us directly or reach out to your cantonal tax authority.

Rental Income

If your secondary residence is rented out, we’re no longer talking about a fictional rent but about actual rental income — that is, the rent you actually receive.

The total amount of these rents must be converted into Swiss francs and reported in your Swiss tax return.

Foreign Real Estate — How does it affect your Swiss tax burden?

After spending about fifteen minutes reading the previous sections, you’re probably eager to get to the heart of the matter: what real impact do your foreign properties have on your Swiss taxes?

The answer could be summed up in one sentence: your properties located abroad affect the tax rates applied to both your income and your wealth.

To make things clearer, let’s look at two examples:

- Example 1: the rule doesn’t exist (a purely fictional scenario)

- Example 2: the rule exists

These examples are based on entirely hypothetical tax rates, used solely to illustrate how the mechanism works. Once you understand this principle, you’ll easily be able to adapt it to your real situation, depending on your canton of residence and the current tax scales.

Explaining the tax mechanism – Simplified example

The headline sums it up quite well. Now it is clear: the country where the property is located will tax you, and Switzerland needs to cope with the standard principle of “no double taxation”, thus should not collect taxes on it as wealth nor on the perceived income.

However, the fiscal and rental values (or the amount of rents) you have provided will allow the authorities to adjust the tax rate applied to your Swiss revenues and wealth. I regret to ruin the atmosphere: it is upwardly adjusted; your tax rate may increase. Let’s illustrate the mechanism with a simple example:

Our example:

- Income generated in Switzerland and taxed in Switzerland (for example your income): CHF 50’000

- Income generated abroad and taxed abroad (rental income): CHF 50’000

Aggregated revenues in 2022: CHF 100’000

To make it even easier, let’s imagine we live in a world where all tax scales are the same (in Switzerland and abroad)

Case 1 – Almost a fairy tale: The rule does not exist

If this was our reality, the tax burden would have been calculated as follows:

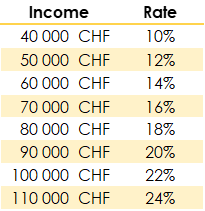

In Switzerland: CHF 50’000 x 12% = CHF 6’000

Abroad: CHF 50’000 x 12% = CHF 6’000

Aggregated tax burden: CHF 12’000 i.e., 12% tax on CHF 100’000.

Case 2 – Reality: The rule exists (unfortunately)

Unlike in above-described idealistic world, taxes are determined as follows:

In Switzerland: They will tax CHF 50,000, not at the rate of CHF 50,000 but at the rate of CHF 50,000 + 50,000 = CHF 100,000. Finally, Switzerland will tax CHF 50,000 at a rate of 22% = CHF 11,000.

Abroad: In most cases, your foreign income will be taken into account to calculate the tax rate: 50,000 x 22% = CHF 11,000.

For a total tax burden of CHF 22’000.

And despite the fact that it may feel unfair, it’s rather logical… If you would have earned it all in Switzerland, the applied rate would have been 22%. Switzerland does not tax the foreign CHF 50’000 but established this rule to restore the “proper” rate, according to the entirety of your annual income.

This first example was meant to showcase the mechanism. I now propose to tackle a more realistic, thus more complex example, adding debts, interests and international distribution to the equation.

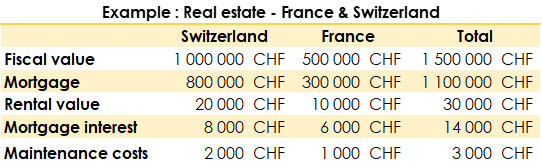

Detailed example — Property in France

The fiscal value of the house I own in the Swiss vineyards was set at CHF 1 million. To finance the purchase, I incurred a mortgage of CHF 800’000, with an interest of CHF 8’000 per year. It costs me an extra CHF 2‘000 annually for maintenance, and the tax authorities agreed to a CHF 30’000 rental value.

My French property has a fiscal value of CHF 500’000, a mortgage of CHF 300’000 for an annual interest of CHF 6’000. The maintenance costs amount to CHF 1’000 per year. Last point, the rental value is CHF 10’000.

First things first: The wealth tax

Step 1: Wealth international distribution assessment

As mentioned earlier, we have to isolate the portion taxed in Switzerland from the one taxed in France.

We have:

- 66.66 % (67%) of our wealth held in Switzerland which will be taxed by Switzerland (CHF 1’000’000 / CHF 1’500’000)

- 33.33% (33%) of our wealth held in France which will be taxed by France (CHF 500’000 / CHF 1’500’000)

Step 2: Determine the international distribution of debt and derive the taxable wealth by country.

While your wealth and income adjust your rate, debt also plays a role. It will decrease either:

- The taxable amount, if it is considered as a Swiss debt.

- The tax rate, if it is considered as a foreign debt.

In our example, we need to distribute the total debt between France and Switzerland. Good news, we will simply have to take the percentages defined in the first step.

Debt allocated to Switzerland: Total debt * Swiss allocation rate: CHF 1’100’000 x 67% = CHF 737’000

Debt allocated to France: Total debt * French allocation rate: CHF 1’100’000 x 33% = CHF 366’667

Thanks to distribution mechanism, we can precisely determine the wealth taxed by each country.

Obviously, after having read (and reviewed, naturally) all our articles related to the calculation of taxable wealth, you know that you can work it with this simple formula: Total wealth – total debt. Back to our example, this translates into:

To conclude, Switzerland will tax the taxable wealth of CHF 263’000 at the global wealth rate of CHF 263’000 + 133’000 = CHF 396’333.

Here we are! We are now clear on how your foreign real estate properties and mortgages will affect your wealth taxation in Switzerland.

Let’s not stop halfway. A few more steps are required to get the full picture. Remember, we need to capture the impact of foreign real estate on your income tax.

International distribution of debts’ interests

In our example, we have leveraged two types of loans (a Swiss mortgage, and a French real estate loan) to finance the purchase of properties. Each of these, in addition to their installments, has a cost taking the form of debt interests.

Each year, interest payments can be deducted from your taxable income. And here again, we need to check what goes where: France, or Switzerland?

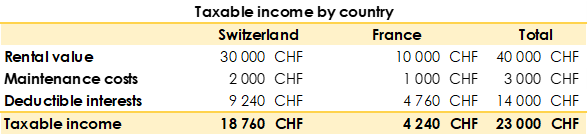

Let’s distribute the CHF 14’000 of paid interest between the two countries, leveraging the wealth allocation performed earlier: 67% to Switzerland, 33% to France

Switzerland will authorize a CHF 9’240 deduction from your taxable income, and France CHF 4’760.

Calculation of taxable income and tax using international apportionment

As easy as ABC now that you master the topic. Take the total taxable income in Switzerland reduced by all the authorized deductions (such as maintenance expenditures), then subtract the interest on the debt, calculated thanks to the international distribution.

In a nutshell, this is the result from our example:

Therefore, Switzerland will tax CHF 18’760 at a rate corresponding to an income of CHF 23’000.

Phew, that was something… What do you think? If you’re still reading these last lines, you probably appreciated this article as much as I did. In case of remaining questions, clarifications or if you simply want to simulate the impact of a real estate purchase, feel free to contact us.

How FBKConseils can assist you with your foreign properties?

Introductory Meeting

At FBKConseils, we offer a free initial consultation designed to clarify any doubts that may remain after reading our articles or watching our videos.

If necessary, we will also take the time to explain how our firm can support you in your financial and tax planning, both in Switzerland and abroad.

Advisory Meeting

This meeting takes place after the introductory consultation. With a flexible duration tailored to your needs, its goal is to answer your remaining questions, perform necessary simulations, and, if required, review the legal basis directly with you during the session. You leave with a clear, complete, and personalized understanding of your situation.

Tax Declaration

Like any fiduciary firm, we offer two approaches:

- Train you to complete your tax declarations, allowing you to gain autonomy and better understand the Swiss tax system.

- Or take care of the entire process on your behalf, saving you time and peace of mind.

Tax Simulations

Buying or selling a property is often a medium- to long-term project. And every project deserves to be examined from every angle: returns, taxation, administrative procedures, financing, etc.

On the tax side, you can engage FBKConseils to perform comprehensive simulations, accompanied by a detailed analysis delivered as a PDF report.