Written by Yanis Kharchafi

Written by Yanis KharchafiFiduciary Expert in Training

HEC/AFA/IAF Graduate

The 12 tax deductions to claim in 2025 in Geneva

Introduction :

Ahhh… Geneva! Its Water Fountain, afterworks, banks and watchmakers … so many delights! And the ones living in this beautiful city know that it has so much more to offer, beyond good cheese and a waterfront favorable to a well-deserved lunch break. What then? Here, we’re talking about the gentle tax headache already looming on the horizon: the 2025 tax return, which will in principle have to be filed during the first part of 2026 (except, of course, for the latecomers).

If the mere prospect of such a mission brings you goosebumps and after careful and repeated considerations, you have concluded this fight will not be yours, that’s fine too: you are not alone. We redirect you straight to the page that will introduce you to our tax return service in the canton of Geneva so that you can better breathe and enjoy your time off.

For all the Rubik’s cube enthusiasts, determined to cross swords with GeTax 2025, this article will help you to identify and understand the main ICC tax deductions to claim according to your situation, and thus limit your tax burden.

But first, a quick reminder. If you have not yet read the previous chapters of our guide on Geneva taxes in 2025, here are some useful links that will shed some light on the calculation of cantonal and communal taxes, as well as wealth tax.

You can also find out about the 15 main tax deductions in the canton of Vaud and in the canton of Valais.

As Michael Buffer would say: Get ready to rumble!

The line-up:

How do tax deductions work in Geneva in 2025?

Before listing and explaining the main tax deductions in Geneva, it is important to set out the theoretical framework, as far too many taxpayers still misunderstand how it works. Except for the self-employed — who are a special case — employees in Geneva (and more generally in Switzerland) must start from their gross salary, which you can find at the beginning of each year on the salary certificate issued by your employer. The goal is then to progressively reduce this gross income in order to obtain several levels:

- Net income, which is your gross salary minus social security contributions (AVS, LPP, LAA, LAAC, IJM). We explain these components in detail in other dedicated articles.

- Taxable income, which corresponds to your net income minus all the tax deductions allowed by your canton of residence. These are the deductions we will review in this article.

- Once your taxable income has been determined, you can enter it into the Geneva tax calculation to obtain your final tax liability.

Even if it may seem obvious, I would like to conclude this first section with an essential clarification: a deduction is not a tax credit. To put it simply, some clients believe that by deducting CHF 3’000 from their income, they will save CHF 3’000 in tax. This is false.

Deducting CHF 3’000 simply means that your taxable income is reduced by CHF 3’000, and depending on your tax rate, this will lower your taxes by between 0 percent and 40 percent of the deducted amount, that is, between CHF 0 and CHF 1’200 in this example.

Now let’s get down to business: what will you be able to deduct in 2026 on your 2025 tax return?

Deduction #1: Business expenses: what can I deduct?

Meals and Transportation Expenses

Regardless of your situation, you can deduct your meal and transportation expenses. Depending on the case, these deductions will be treated separately or, if you live close to your workplace, combined into a single lump-sum allowance. We explain all of this in more detail below. We have chosen to address both items together because they rely on the same fundamental choice: do you want to use the actual-expense method or the lump-sum method?

This first group of deductions is based on the LI-PP (Law on the Taxation of Individuals), Article 29, paragraphs a) and b).

Actual business expenses

The tax authorities allow you to deduct, under certain conditions and within certain well-defined limits in Geneva, the expenses generated by the simple fact that you have a job and that you must, in most cases, get to the office on a regular basis. This includes:

- Business expenses: transportation expenses

In the Geneva canton, in 2025, travel expenses are strictly limited to CHF 534 per year. Whether you use the new electric bike you bought to accommodate your physical or ecological awareness, your car to commute from Hermance to Versoix every day, or public transportation: the maximum deduction authorized by the canton and your municipality will be CHF 534, not a single cent more. On the other hand, if your employer contributes to your transportation costs, you will not be able to benefit from this deduction (this is the case if a cross appears in the “F” box of your salary certificate).

Please note that this threshold, like many others, differs when it comes to the direct federal tax (IFD), which limits this deduction to CHF 3’300 per year and can vary depending on the means of transport you use.

- Business expenses: meal expenses

Here again, the conditions are relatively strict compared with other cantons: the deduction of meal expenses will only be accepted if the TPG does not allow you to make the ‘work-home’ journey in less than 30 minutes. Long story short: if you live within 30 minutes (one way) from your workplace, forget about the meal expenses deduction.

Otherwise, you will be able to deduct CHF 15 per day up to a maximum of CHF 3’200 per year for meal expenses incurred outside of your home, provided that your employer does not contribute to it. If in doubt regarding your employer’s contribution, you can always refer to your salary certificate: a check marked in box “G” on your salary certificate will halve the allowed deduction to CHF 7.50 per day, for a maximum of CHF 1’600 per year.

Flat rate business expenses

The canton of Geneva offers an alternative for those who live close to their place of work: the deduction of a lump sum for professional meals and transportation expenses. This amount will range from CHF 640 to CHF 1’812 for all salaried individuals, and will depend on the gross salary, reduced by the AVS / AI / APG / Unemployment / AANP / Amat contributions and those of the 2nd pillar – all of which are detailed on the salary certificate.

Grab your calculator!

- Take your total gross salary – box 8

- Deduct the sum of the above-mentioned social contributions (boxes 9 and 10.1)

- Multiply it by 3%.

What do you get? Remember, the minimum is CHF 640, which means that even if the result is lower, tax authorities will admit a CHF 640 deduction. The same goes for the maximum, so if it is greater than CHF 1’812, you will only be entitled to the maximum lump sum deduction of CHF 1’812. Between these two thresholds, the amount obtained will be deductible as is.

Obviously, you can either claim a lump-sum deduction or deduct the actual expenses, if properly documented. Remember to check which of these options is the most suitable for you and… If you have any questions, just contact us!

Business expenses: Other Actual Expenses

In addition to transportation and meal expenses, some employees incur other costs in order to carry out their professional activity. With the appropriate supporting documents, you may be able to deduct, for example, your union dues, as specified in the tax guide, as well as work clothes and other items required for your job, provided your employer does not supply them.

Another deduction often overlooked by taxpayers in Geneva , yet also part of this first category of professional expenses, concerns… rent. Surprising, isn’t it? Yes! But be careful: deducting part of your rent is subject to strict conditions:

- Carry out your professional activity from your home, in other words, not work in an office.

- Not having a professional workspace provided by your employer. If you simply have the option of working from home but choose to stay there for personal comfort, the deduction will not be accepted: it must be a constraint, not a choice.

- Have a genuinely dedicated workspace in your home. In principle, if your “office” is set up in your bedroom or living room, it will be difficult to justify that your rent includes an additional living area specifically intended for your work. You must be able to demonstrate that you chose a larger apartment than necessary in order to perform your professional activity there.

If these conditions are met, you may deduct a portion of your rent, calculated in proportion to the surface area of your workspace relative to the total surface area of your home.

Deduction #2: Health and accident insurance premiums

It is widely known that for most households, after rent (which we attempted to deduct in the previous section), health insurance premiums represent one of the largest annual expenses.

Good news for Geneva residents: to our knowledge, the canton of Geneva offers the most generous health-insurance tax deductions in French-speaking Switzerland. Depending on your age bracket and the number of dependants you have, you will be able to deduct the following amounts in 2025, in accordance with Article 32 of the LIPP:

- Children (ages 0 to 18): CHF 3’965

- Young adults (ages 18 to 26): CHF 12’842

- Adults (over age 26): CHF 17’122

Be careful, however: if an adult pays both mandatory and supplemental health insurance for a total of CHF 600 per month (i.e., CHF 7’200 per year), they will not be able to deduct CHF 17’122, but only the amount actually paid, in this case, CHF 7’200. In conclusion, despite the steady increase in premiums year after year, in Geneva, the entirety of your health insurance premiums, as well as those of your children, should remain fully deductible in 2025.

You can find all deductible amounts in the tax certificate(s) issued by your health insurance provider at the beginning of each year. For several years now, these documents have no longer been sent by post but are available directly in your insurer’s online customer portal or mobile app.

Deduction #3: Medical expenses

All too often, we still see taxpayers confusing health insurance premiums (paid each month and described in the previous section) with unreimbursed medical expenses. It is important to clearly distinguish between the two.

Among the deductible medical expenses, you may include the following:

- The annual deductible: when you take out health insurance in Switzerland, the first francs spent each year remain at your expense. Since this deductible is never reimbursed, it is fully considered part of your deductible medical expenses.

- The coinsurance (quote-part): without going into all the details of the system, once you have reached your deductible, you must still cover a share of the costs, generally between CHF 0 and CHF 700 per year.

- “Necessary” treatments not covered by mandatory health insurance or your supplemental insurance: among the most common are dental care, eyeglasses, non-reimbursed medication, and expenses related to IVF (in vitro fertilization).

It is the total amount of these expenses, in other words, what you actually paid out of pocket, that constitutes your deductible medical expenses for the tax year concerned. These amounts generally appear on your health insurance tax certificate.

The question now is the following: once your medical expenses have been determined, what can you actually deduct?

In Geneva, you are allowed to deduct the portion of your actual medical expenses that exceeds 0.5% of your net income, after taking the other deductions into account.

Let’s take a practical example:

- Start with your net salary, which is your gross salary minus the AVS and LPP contributions.

- Then deduct, if applicable:

- your 3rd pillar A or B contributions, as well as your LPP buybacks,

- your professional expenses (actual or lump-sum),

- your health and accident insurance premiums,

- your childcare expenses.

- Multiply the amount obtained after these deductions by 0.005 (that is, 0.5%). This result represents the minimum threshold that applies. In other words, if your medical expenses are below this amount, they will not give you any right to a deduction. However, anything that exceeds this threshold will be deductible from your income.

In conclusion, the maximum deduction allowed corresponds to the difference between your actual medical expenses and the threshold calculated in the previous step.

Deduction #4: The pillar 3A – Tied private pension provision

Next, let’s focus on what is considered to be the most elementary tax optimization, the pillar 3A. There is a wide range of products available and promoted on the market, of which you have surely heard about. Before we deal with the deductions related to this voluntary contribution, let’s quickly check: you still think that the “A” stands for “Assurance” – Insurance, in French? If so, let’s pause here and get back to basics. We recommend that you first visit this page, which will remind you of the fundamentals of the 3rd pillar A. Once comfortable with key notions, the question of the contributions naturally arises, and here again grab your hand to deep dive. And for those who prefer a short video summary in under four minutes, you’ll find it here.

The major strength of the pillar 3A is that it is deductible. Indeed, whether it is concluded with a bank or an insurance company, it combines a number of advantages, all of which are easily and instantly measurable. Let’s start with the mechanism:

- You can freely choose the amount you wish to contribute annually, and, as an employee, it can be deducted from your taxable income as long as the amount doesn’t exceed CHF 7’258 per year (Incidentally, this amount is the maximum in 2025, which was adjusted upwards in 2023). First good point.

- For self-employed individuals or employees who do not contribute to the 2nd pillar, the maximum deduction amounts to CHF 36,288 or 20% of annual income.

- From a wealth taxation perspective, it’s pretty simple. The capital saved over the years is not taxable and thus “disappears” from the tax authorities’ radar until you decide to withdraw your 3rd pillar.

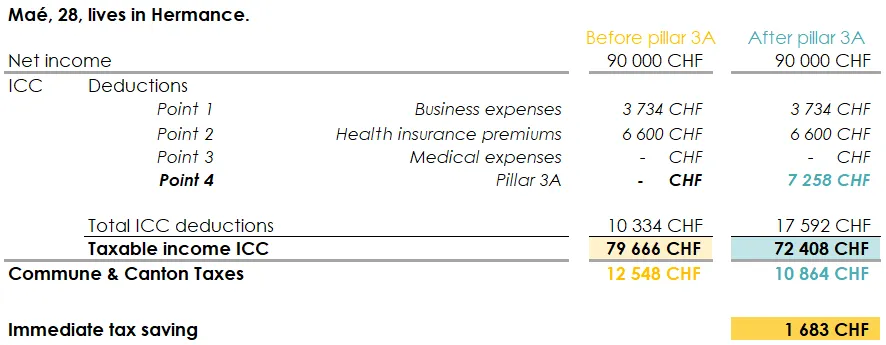

As promised, let’s quantify this with an example focused on cantonal and communal taxes (ICC):

For her 2025 tax return, Maé decides to take the bull by the horns and look into her situation a little early, but not too early, let’s say in early November 2025. Following a salary increase, she realizes she is now able to save a few extra hundred francs each month. Without contributing to the 3rd pillar, her taxable income would be approximately CHF 79,666 and she would pay CHF 12,548 in income tax (excluding federal direct tax).

Like many of us, she has heard about the possibility of allocating part of her savings to a 3rd pillar A, which she will be able to access when she retires or if she later decides to purchase her primary residence. For this year at least, she chooses to go with a banking product. Before making the payment, she asks us to simulate the impact of her decision. Time to get our calculators out!

By allocating part of her savings to a 3rd pillar A during the year 2025, she reduces her taxable income by CHF 7’258, bringing it down to CHF 72’408. As a result, her taxes also decrease and her final cantonal and communal tax bill comes to CHF 10’864, which is CHF 1’683 less than if she had kept her savings under her pillow. Seen from another angle, this represents a return on investment of 23.2%. Quite interesting, isn’t it? And that is without counting the fact that the deduction also applies at the federal level, which is even better.

This is also a good opportunity to illustrate how much your personal situation can affect your tax burden. For a moment, let us imagine Maé as a separated mother with one dependent child, and with the same taxable incomes, that is CHF 79’666 before the 3rd pillar A and CHF 72’408 after it.

With one child and without the 3rd pillar A, her tax burden would amount to CHF 9’012, whereas with the 3rd pillar A it would drop to CHF 7’300, resulting in a tax saving of CHF 1’712. Conclusions?

- The tax saving you can make with a 3A (or any other additional deduction) depends mainly on your marginal tax rate: the higher your marginal tax rate, the greater the saving.

- Beware of advisers who claim to be able to save you the same amount of tax as your neighbour, with the same product, without having any knowledge of your tax situation. Every situation, including your own, is unique, and yet it’s not uncommon to be approached by ‘soothsayer advisers’.

Deduction #5: The Pillar 3 B

Because it is deductible in the canton of Geneva specifically, the pillar 3B has strong potential too, because the premiums paid also give entitlement to a deduction. The maximum amount depends on your employment status as well as your household’s composition. For employees, figures listed below can be added up to know the total deduction that could be granted in 2025:

- Single person: CHF 2’345

- For a married couple or a couple in a registered partnership: CHF 3’518

- Per dependent child: CHF 959

In cases where only one member of the household is employed, or where the household consists of self-employed individuals who are not affiliated with a 2nd pillar, the amounts increase, providing greater deductions.

Once again, FBKConseils would like to warn you: just because a product is tax-deductible does not necessarily mean it is a good financial opportunity. The 3rd pillar B consists of insurance products that still today involve fees that are often too high, whether management fees, brokerage fees or early-exit fees.

In our view, except in very specific cases, these products are likely to make you lose more money than you would save through the tax deduction.

Our advice is simple: stay cautious whenever you hear the word ‘insurance’!

Deduction #6: LPP years buyback

Another aspect of retirement planning in Switzerland involves deducting the capital allocated to your second pillar. Here, we are not referring to the usual contributions that you and your employer contractually make to your 2nd pillar, but rather to an individual and optional choice to bridge a gap, created over time in your 2nd pillar.

Each franc invested today for your later years is, without upper fiscal limit, deductible from your taxable income and will allow you to reduce your tax burden for the current year.

But beware, although attractive, some fundamental notions must be understood before proceeding with this type of mechanism. First of all, make sure you understand your LPP certificate in order to identify the magnitude of potential buybacks, and the optimal timing. If necessary, our comprehensive guide to 2nd pillar buybacks is available for consultation.

Few doubts remain as to how the Swiss pension system works and you are not yet comfortable with the terminology of the second pillar? These definitions should clarify it all.

Deduction #7: Third-party childcare expenses

No grandparents nearby and a full-time job?

If you need to rely on third parties to look after your child or children under the age of 14 to work or follow a training program, you can deduct these expenses up to CHF 26’320 per child per year (2025 amount).

For married couples or registered partners, this deduction is only available if both spouses are working, in training, unemployed or in a long-term incapacity to work.

Deduction #8: Alimony payment

Life is not always a smooth ride, and sometimes paths diverge. We will spare you the details. If you pay alimony or maintenance contributions to your ex-spouse, whether for them or for your children, here is a small consolation: the full amount is deductible for you.

In 2025, however, we observed many interpretation issues on this topic.

This deduction, which may appear simple at first glance, can become a source of disagreement with the tax authorities if certain precautions are not taken. During a separation, even when the relationship remains amicable, it is crucial to put things in writing. If you decide to pay the children’s health insurance premiums, their holidays or other day-to-day expenses without a clear agreement, it will be difficult for the tax authorities to determine whether these payments truly constitute alimony or simply occasional assistance, or even a gift.

Our recommendation is the following: define precisely and in writing who pays what, for whom and on what basis.

Deduction #9: Interest on debts, whatever their nature

Without really knowing why, we had skipped this deduction in the previous versions of this article, even though it is often misunderstood. It was therefore time to give it the place it deserves in this new update.

In Geneva, as everywhere else in Switzerland, it is possible to deduct all the interest paid on your debts, and this until 2028, virtually without any limit. In practice, the law does set a ceiling, but for 99.99 percent of taxpayers it will never be reached, so we can forget about it for now.

What types of interest are we talking about exactly?

- Mortgage interest: When you purchase real estate, whether in Switzerland or abroad, it is common to use a bank or financial institution to finance part of the property. In return for the funds lent, the institution charges you interest, which may vary depending on the type of loan. These mortgage interest payments are fully tax-deductible.

- Interest on consumer loans (unsecured debt): This is where many taxpayers tend to forget items. Many people take out this type of loan at some point, whether to finance their children’s studies, buy a vehicle or simply pay for online purchases through a credit card. All these “small” loans include an interest component, and that component can be deducted from your income, thereby reducing your tax burden.

- Tax debts: Even more surprising, and almost always forgotten, debts owed to the tax authorities can also give entitlement to a deduction. In Switzerland, it is not rare to have underpaid your tax instalments, for example in the event of an unexpected bonus, a job change or a divorce during the year. If, on 31 December 2025, you still owe part of your taxes, the administration will likely charge late-payment interest. These interest payments can also be deducted in your tax return, just like the others.

Deduction #10: Banking fees

Another Geneva-specific feature, and this time a positive one. In Geneva, as everywhere in Switzerland, you are entitled to deduct banking fees, meaning deposit fees and account maintenance fees. We agree that, taken individually, these amounts are not huge, but when added together, especially if you have several banking relationships, they can represent a significant sum. This is even more common for people coming from abroad, who often keep bank accounts in several countries.

The Geneva-specific feature lies in the treatment of asset management fees. The canton allows a portion of the management fees incurred to generate investment returns to be tax-deductible.

Among these fees, we can include in particular:

- Custody fees and ordinary fees for the administration of securities held with a financial institution,

- Management fees, deductible up to 50 percent,

- Integrated fees (flat fees or all-in fees), deductible up to 45 percent,

- Safe deposit box rental fees,

- Fees for obtaining tax statements.

Let us be honest: it is often difficult to draw a perfect line between what is deductible and what is not. This is why our recommendation is simple: request the deduction of all the fees you have actually incurred and let the tax authorities carry out, where necessary, the sorting and precise calculation of what can effectively be allowed.

Deduction #11: Family allowances

In the canton of Geneva, as you will have noticed, the same tax scale applies to everyone who is taxed under the ordinary system, without distinction. In addition to the full or partial splitting we explained here, the family charge deduction is a social deduction designed to rebalance taxation and allow those who support children to reduce their taxable income (a bit more serious all of a sudden). All right, but how much are we talking about?

This will depend on the number of full and half tax charges allocated to your household:

- In 2025, for individuals who have not claimed any childcare expense deductions (you can already sense the other side of the coin coming), the lump-sum amount is CHF 13’660 per full charge and CHF 6’830 per half charge.

- However, if you occasionally entrust your children to third parties and claimed the deduction for the related expenses under point 7, then the limit is set at CHF 10’412 per full charge and CHF 5’206 per half charge. Note that these latter amounts are those of 2024 and will be updated once the new figures are published.

A quick aside: what exactly is a family charge?

First of all, a family charge refers to a dependent child for whom you provide support. Whether the child is a minor or in vocational training or studying, the determining factor is their income. In 2024, as long as this income was below CHF 16’197, you were granted a full charge for each child meeting this condition. A half charge applies when the child’s income is between CHF 16’197 and CHF 24’296 and when the adult child’s assets do not exceed CHF 92’432, or when separated or divorced parents share the child’s support equally without paying alimony to one another.

This applies to children, but also to other dependants.

Deduction #12: Dual-income spouses

This special deduction is granted to couples (married or in a registered partnership), and more specifically to the spouse with the lower income. The good news is that this person can deduct CHF 1’051 from their taxable income, as long as their activity is not connected to that of the higher-earning spouse.

If you have made it this far, it means you are now starting to accurately simulate what your 2025 taxable income will be when filing in 2026. Nevertheless, as practical as this guide may be, it does not take into account every possible deduction. It simply presents the most important ones.

How can FBKConseils support you with your tax questions in Geneva?

A free introductory meeting:

At FBKConseils, including in 2026, we continue to offer a first meeting free of charge, lasting around twenty minutes. Its purpose is simple: to answer all your tax-related questions. And if you would like to know more about our way of working or about our services, we will use this meeting to provide you with further information.

Training to declare your income and assets:

One of the specific features of our firm is that we offer our clients personalised training to learn how to complete their own tax return. This approach allows you to gain autonomy while better understanding the Geneva tax system, so that you can optimise your situation in the future.

Full delegation of your tax return:

More traditionally, FBKConseils offers a turnkey service for the full handling of your Geneva tax return. Thanks to our online platform, you can obtain a personalised quote, generate the exact list of required documents and upload all your files directly on our website. This service begins with an introductory meeting, continues with the sending of successive versions of your tax return and ends with the final submission of your return to the tax authorities, in your name and according to your approval.

Personalised tax simulations:

In addition to our standard services, we offer our clients forward-looking tax simulations to anticipate life changes and optimise their financial decisions. These simulations can cover a wide range of areas, such as LPP buybacks, marriage or divorce, property purchases in Switzerland or abroad, or the creation of a business.